Mortgage revenues remain stagnant despite jump in CPF

While Southold Town’s community preservation fund revenues returned to pre-recession levels in 2013 — as reported last week — the amount of money the town collected in mortgage taxes last year remained stagnant.

Unlike the CPF, which gets 2 percent of all real estate transfers in town above $250,000, mortgage tax revenues require, well, mortgages.

“The [real estate] market seems robust,” said Southold Supervisor Scott Russell. “But it would appear from the numbers that nobody’s asking for, or the banks aren’t approving, mortgages. The mortgage revenues we’re receiving are still where they were during the depths of the recession.”

Those revenues, depending on the amount, could be a healthy chunk of the town’s now $31 million operating budget, which doesn’t include the CPF fund or special districts like solid waste. (The town’s overall budget is $41.6 million.)

Because personnel costs are the biggest expense for local governments, the town has left about a dozen positions unfilled since mortgage revenues plummeted in 2008, Mr. Russell said. The town also had to ask for, and received, concessions from the CSEA union, which represents most of the town’s non-police employees.

Because personnel costs are the biggest expense for local governments, the town has left about a dozen positions unfilled since mortgage revenues plummeted in 2008, Mr. Russell said. The town also had to ask for, and received, concessions from the CSEA union, which represents most of the town’s non-police employees.

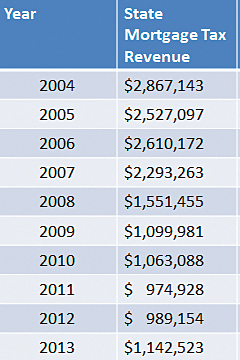

The highest level of mortgage tax revenue Southold Town received in the past decade came in 2004, when it collected about $2.9 million. That number dropped to $1 million in 2009 — down from $1.5 million in 2008 — and has hovered around that mark ever since. The town collected $1.1 million in 2013, up slightly up from $990,000 in 2012 and $975,000 in 2011.

“It’s a pretty substantial loss,” Mr. Russell said. “It shows you the difficulty we’ve been trying to wrestle with to keep the tax levy below 2 percent.”

As for the real estate market, realtor Marie Beninati, co-owner of Beninati Associates in Southold, said several high-end waterfront properties changed hands in 2013.

“And generally, a number of those big deals end up being cash or mostly cash, maybe half,” she said. “It’s a combination. Yes, there are more cash buyers, but they’re also financing less on the larger sales. Generally, someone who’s buying a $2 million house is not financing 80 percent. So there’s more cash there and less mortgage.”

Most second-home owners tend to borrow less, she said.

Kevin Santacroce, an executive vice president and chief lending officer at Bridgehampton National Bank, said the bank has noticed that “the demographics of the purchaser are changing” in the town.

“It is not that banks are not approving mortgages,” he said, “it is that most of the real estate buyers are paying cash, because they can afford to.”

Mr. Russell said he’ll have to continue to budget for about the same amount each year until things change.

“I look at the performance over the past few years and if you’re not seeing much of a change in the performance then I’m not going to make much of a change in what I’m allocating,” he said.

Neighboring Riverhead is also dealing with a prolonged stagnation in mortgage tax revenues — down from $3.1 million in 2006 to about $1.2 million in 2013. Riverhead’s Community Preservation Fund revenues have not yet rebounded to the levels that existed before the economic downturn began.

Mortgage tax revenues in Riverhead rose slightly over the past three years.

“In Riverhead we are planning for a conservative increase in mortgage tax each year moving forward,” said Supervisor Sean Walter, a real estate attorney. “My predictions are based on several factors, including the number of real estate transactions I have in my private law office. I see growth, albeit slow growth.”