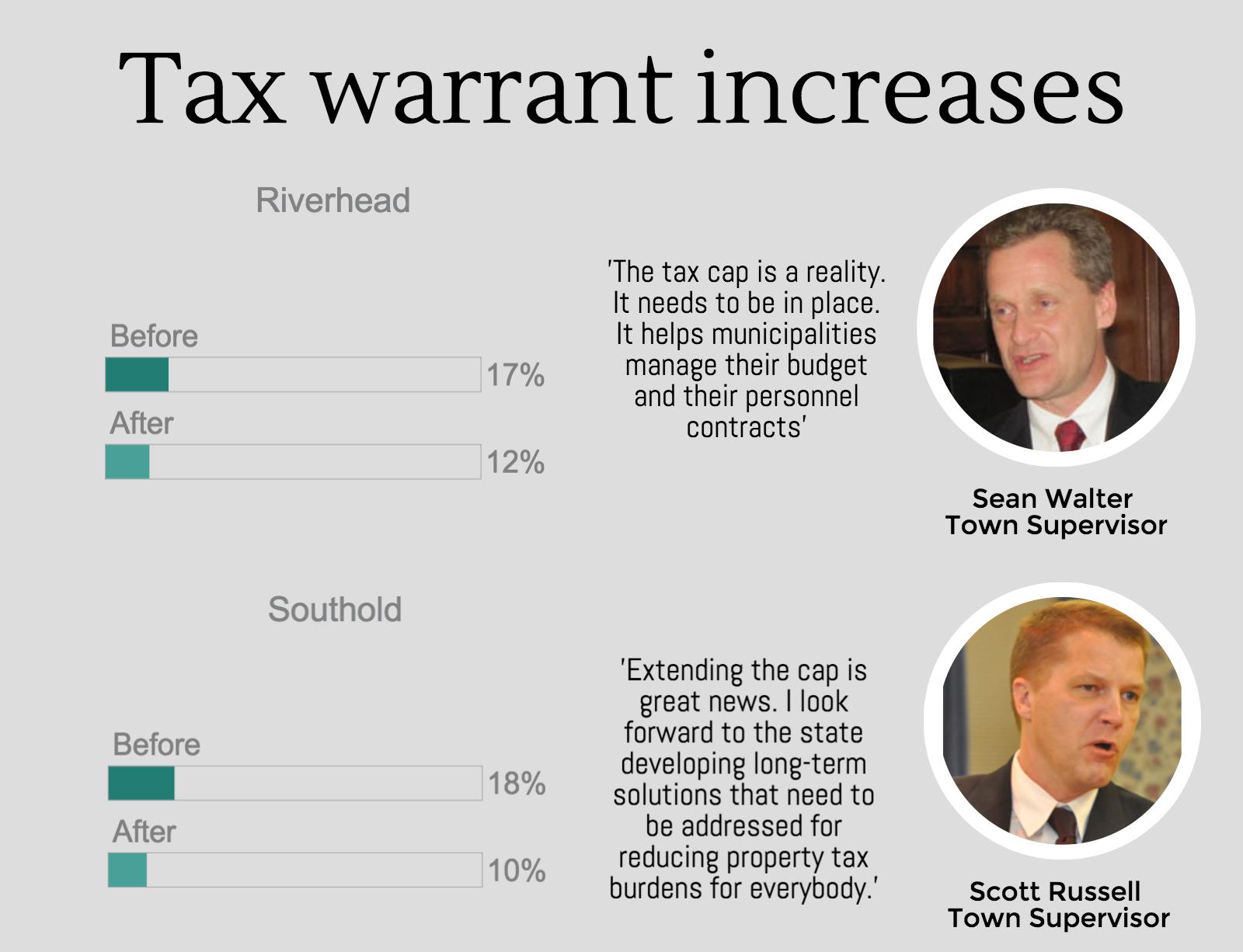

Four years later: A local analysis of the 2-percent property tax cap

With news late last month that the New York State Legislature extended the 2-percent property tax cap another four years, we took a look back at the property tax warrants — the amount of property taxes collected by the town each year, including school, town, county and other taxes — in the two North Fork towns to see if taxes had increased at a lesser rate since the law was enacted.

We found that not only had the tax warrant increased at a slower pace in Southold and Riverhead towns since 2012, it did so at a significant rate.

Below is the percentage by which the tax warrant increased overall in each town in the four years before the law was enacted and in the four years since:

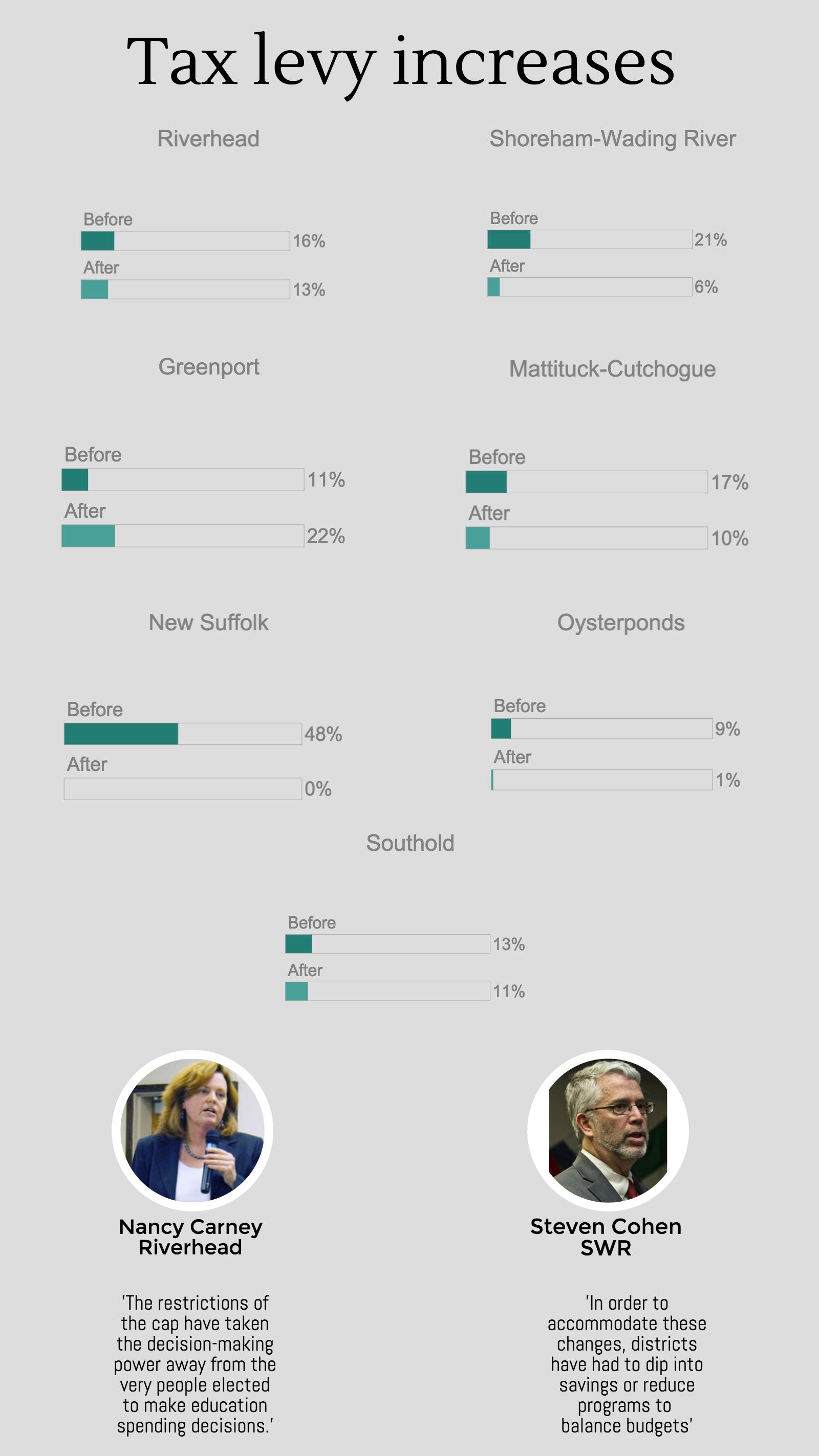

Bu not everyone is in support of the tax cap extension.

Local school officials say having to manage their budgets within the constraints of the property tax cap has caused problems within their districts.

And the rate to which property tax increases have declined since the cap was enacted has not been as steep with most local school districts as it has other municipalities.

In fact, one district, Greenport, has seen more of an increase in its tax levy these past four years than it did in the four years prior.

Below is the percentage by which the tax levy has increased overall in each district in the four years before the law was enacted and in the four years since:

A Sierra Research Institute poll released in May reported that 73 percent of the 695 registered voters polled agreed that the tax cap accomplished what was intended in that property taxpayers are not seeing large annual increases.

The survey also found that 43 percent favored keeping the tax cap as it is, 36 percent favored keeping it but with changes to give school districts and local governments more flexibility to increase property taxes, and only 17 percent favored eliminating it.

Meanwhile a research and data report from the Empire Center for Public Policy, which describes itself as “an independent, non-partisan, non-profit think tank based in Albany, New York,” found that since the tax cap went into effect, school tax levies have risen by an average of just 2.2 percent annually—the lowest in any four-year period since 1982.

The tax cap was first enacted in June of 2011 and limits the percentage a tax levy can rise to two percent or the cost of living, whichever is less.

It applies to all school districts and local governments, including counties, towns, villages and special districts, such as fire districts.

The tax cap also includes some exemptions, such as school capital projects, pension increases over two percent and civil “tort” awards against a municipality.